Blockchain & Cryptocurrency , Cryptocurrency Fraud , Fraud Management & Cybercrime

US Lawmakers Continue Push for Stablecoin Regulations

Congress Weighs State-Level Laws, Identity Concerns at Virtual Hearing

U.S. Department of the Treasury Under Secretary for Domestic Finance Nellie Liang was the sole witness during a House Committee of Financial Services hearing on digital assets this week. In it, members of Congress discussed the overwhelming demand for regulation along with lax cybersecurity controls often pegged to crypto platforms.

See Also: OnDemand | NSM-8 Deadline July 2022:Keys for Quantum-Resistant Algorithms Implementation

In the four-hour hearing entitled "Digital Assets and the Future of Finance: The President's Working Group on Financial Markets' Report on Stablecoins," lawmakers covered areas related to cybersecurity, specifically conversation around safe measures to validate the identity of crypto asset holders and how regulatory actions could further prevent some illicit activity, including money laundering, connected to cybercrime.

"The digital asset space, while built on a new technology offering the potential for innovation, also carries some risks to consumers, users and investors," said Liang. "The market regulators … are taking actions to try to reach consumers and investors. And I expect these actions will continue as they address fraud, misleading advertising [and] manipulation."

Liang pointed to the President's Working Group report, which addresses key concerns about the risks associated with stablecoins, which are virtual currencies pegged to fiat currency, including the U.S. dollar. The PWG report was released in 2021 and predominantly analyzes the risks, including the possibility of a "run" on stablecoins and implementing federal oversight for wallet issuers, which in part may account for improved cyber hygiene.

While the PWG report called only for federal oversight, other legislators recommended state-level action.

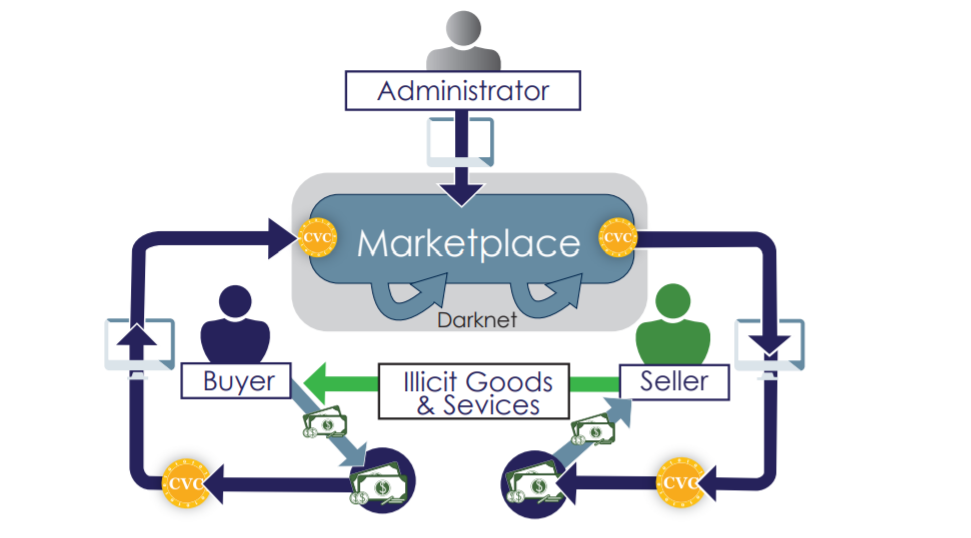

Other members of Congress discussed the lack of know-your-customer controls, which could spur money laundering of ransomware proceeds or other criminal activity. Rep. Warren Davidson, R-Ohio, called Tether, a top-ranking New York-based stablecoin trading exchange, a "time bomb," if it continues to go unregulated.

Liang, who has been advocating for similar regulations for months, was consistent in her position that more legislative guidelines must be put forth if stablecoins are to become a larger part of the financial system (see: Treasury Official Urges Congress to Regulate Stablecoins).

State vs. Federal Regulations

Rep. Patrick McHenry, R-N.C., said regulating stablecoins remains a "bipartisan" task and that that many legislators have called for regulations to rein in volatile, perhaps unsecure tokens. He also called for regulation at the state level, empowering state regulators to act on questionable crypto activity occurring within its borders.

"These issuers are subjected to a comprehensive set of super visionary regimes, including reserve requirements, examinations, compliance with anti-money laundering rules - and that's being done in a couple of states," McHenry said. "We should be examining all existing frameworks, regulatory frameworks and structures for best practices and taking advantage of the lessons learned from those operating on the forefront at the state level."

"We know that New York is the most active and they have a very, very safe but very robust set of regulations [for digital assets]," he added, and he called for a comprehensive study of state-level actions on digital currencies.

The National Conference of State Legislators, an organization with a mission to increase cooperation at all levels of lawmaking, provides a full listing of all state-level cryptocurrency regulations.

Secure ID Standards

Rep. Bill Foster, D-Ill., described the danger of unregulated cryptocurrencies, saying these platforms operate without a complete view of who their customers are. The danger, he said, includes money laundering for ransomware gangs, human trafficking and other nefarious dealings.

"We must have a legally traceable identity to the … owners behind the transaction that can be executed in a court in a trusted jurisdiction, in a country that we have extradition treaties with," said Foster. He cited recent hearings in which "crypto billionaires" essentially agreed that know-your-customer controls are a necessary condition for crime prevention.

Despite the challenges, Liang told lawmakers that the "rapid scalability" of stablecoins is a promising feature.

Foster said he remains curious about the Financial Crime Enforcement Network's position on wider programs to confirm identity for crypto accounts.

FinCEN Responds

Jayna Desai, director of the Office of Strategic Communications at FinCEN, tells ISMG that in recent years the agency has released two advisory statements pertinent to the discussion by Foster: one about the risk of ransomware, updated in Nov. 2021, and the other about illicit activity related to virtual currency, released in May 2019.

Desai says: "Most administrators of stablecoins already have obligations under the [Bank Secrecy Act] and most are also already registered as [Money Service Businesses] with FinCEN."

There are some clear signs, Desai tells ISMG, that a virtual currency platform is compliant. One includes registering as an MSB with FinCEN and avoiding entities that may have ties to questionable activity, or those sanctioned by the federal government, according to FinCEN's "Advisory on Illicit Activity Involving Convertible Virtual Currency."

Ransomware operators, for instance, may rely on money launderers using unregulated, decentralized crypto platforms or mixers to obfuscate funds.

A 'Ticking Time Bomb'?

The popular platform Tether has also been the focus of increased scrutiny of late.

In a Bloomberg Businessweek report about the platform's shortcomings, authors wrote that Tether "broke just about every rule in banking."

Tether did not immediately respond to ISMG's request for comments about its business practices and security measures.

In recent months, ISMG has reported on a series of breaches related to cryptocurrency platforms, showing just how prevalent digital assets are among today's cybercriminals (see: $4.4 Million Stolen From Crypto Firm: Multi-Bridge Exploited; DeFi Platform Qubit Finance Hacked for $80 Million).

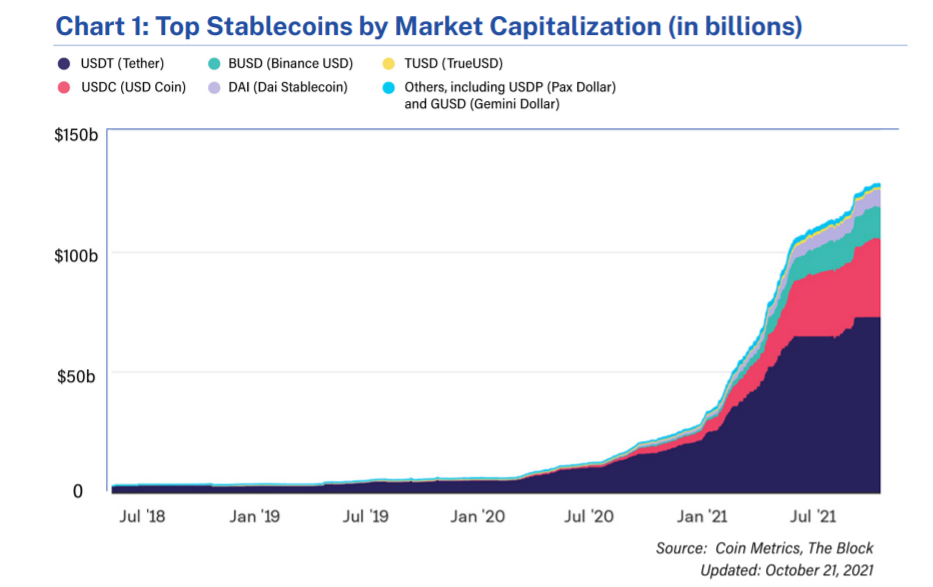

While interest in Tether has declined, according to reports by Fitch Ratings, interest in stablecoins has grown by 450% in 2021. The market has reached $156 billion in total locked value, as of Dec. 2021.

Many blockchain security experts contend that cryptocurrency is not a problem in itself but does carry a cybersecurity flaw. Still, many blockchain experts say, it is becoming increasingly difficult to launder stolen digital assets, since the public ledger on which the transactions take place is immutable.

This was illustrated in this week's shocking news about a New York couple that was arrested for allegedly laundering $3.6 billion connected to a 2016 hack of the platform Bitfinex. Law enforcement authorities praised other crypto platforms for their cooperation in the case (see: Bust of Cryptocurrency Couple Shows Money Laundering Risks).